Curve v2 CryptoSwap: exchange and fee

By 0xstan & 0xmc

Curve v2 CryptoSwap: exchange and fee

Curve v2 CryptoSwap 详解系列:

- Curve v2 CryptoSwap: white paper

- Curve v2 CryptoSwap: add and remove liquidity

- Curve v2 CryptoSwap: exchange and fee

- Curve v2 CryptoSwap: repegging

- Curve v2 CryptoSwap: math lib

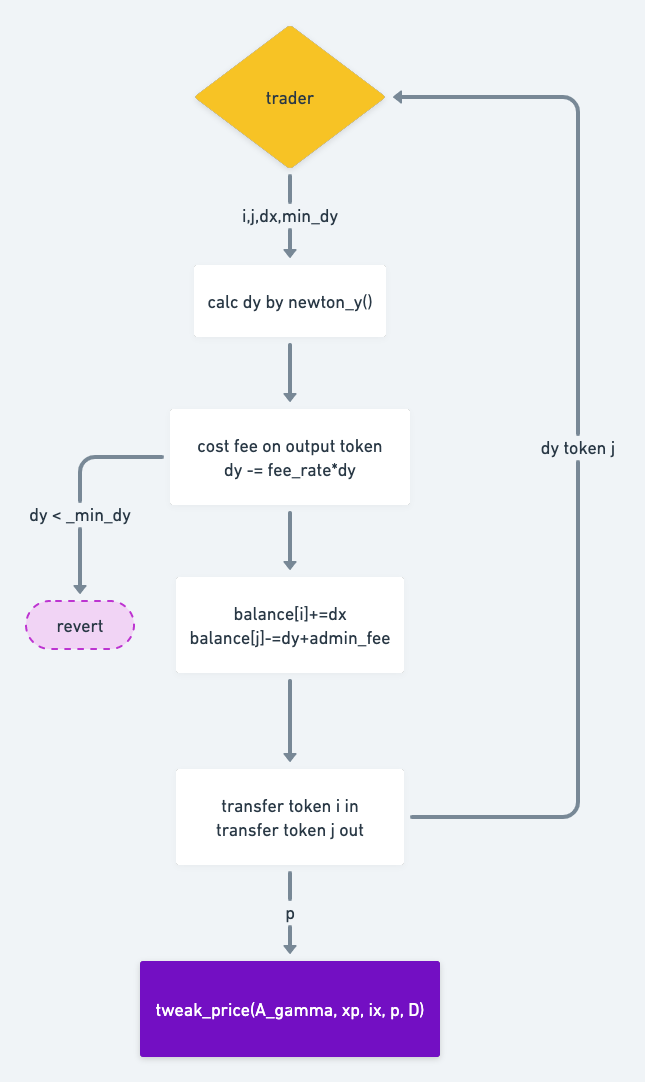

exchange

交易的逻辑相对于流动性的操作较为简单,与 Uniswap 的 exactInput 接口类似,指定输入的 token 数量,和预期最小的输出数量。

其不同之处在于两者计算输出数量所使用的平衡公式不同,由于 Uniswap 的公式相对简单,可以直接求解析解,而 Curve 的核心公式更加复杂,无法直接求出解析解,需要借助牛顿法迭代求解。有关牛顿法的详解解析可以参考我们之前的相关文章:

- 英文版 Reference and Innovation of Newton's Method Code

- 中文版 curve V1&V2 牛顿法代码思路及借鉴创新-(对 curve math 库做科普)

exchange 的函数接口如参分别是输入资产 i 数量 dx,输出资产 j,输出数量不能少于 min_dy,返回实际的输出数量。

- 检查入参,资产序号合法,输入资产数量 > 0

- 转入输入资产

- 取出 A 和 gamma 系数,如果处于调整期,需要线性计算其值

- 不考虑手续费的情况下,利用

newton_y计算出交易后池子内输出资产的 xp,和交易前的 xp 相减,得出输出 dy,更新全局变量 xp, balances- 注意

newton_y计算的结果是价值 (和 xp 同单位),不是数量 (balance) dy / price_scale[j]价值 / 价格 得到数量,由于不同 token 的 decimal 可能不同 (不都是 18,例如 USDC 是 6),所以还要乘以 precisions 变量

- 注意

- 转出输出资产

- 根据 dx dy 计算该笔交易的实际执行价格, 带入 tweak_price 逻辑 (repegging)

@payable

@external

@nonreentrant('lock')

def exchange(i: uint256, j: uint256, dx: uint256, min_dy: uint256, use_eth: bool = False) -> uint256:

assert not self.is_killed # dev: the pool is killed

assert i != j # dev: coin index out of range

assert i < N_COINS # dev: coin index out of range

assert j < N_COINS # dev: coin index out of range

assert dx > 0 # dev: do not exchange 0 coins

A_gamma: uint256[2] = self._A_gamma() # cache A and gamma

xp: uint256[N_COINS] = self.balances # xp container, cache balances, will multiply price later

ix: uint256 = j # the index of output coin

p: uint256 = 0 # init price of exchanging

dy: uint256 = 0 # init amount_out

if True: # scope, simular with {} in solidity

_coins: address[N_COINS] = coins

if i == 2 and use_eth: # Using eth, msg.value as amount in, then trans ETH to WETH

assert msg.value == dx # dev: incorrect eth amount

WETH(coins[2]).deposit(value=msg.value)

else: # msg.value must be zero when exchaging without eth

assert msg.value == 0 # dev: nonzero eth amount

# assert might be needed for some tokens - removed one to save bytespace

ERC20(_coins[i]).transferFrom(msg.sender, self, dx)

y: uint256 = xp[j] # cache token_out's reserve

x0: uint256 = xp[i] # cache token_in's reserve

xp[i] = x0 + dx # dx is amount_in, xp is still balances, not balance*price

self.balances[i] = xp[i]

# cache price_scale multiply balance get xp

price_scale: uint256[N_COINS-1] = empty(uint256[N_COINS-1])

packed_prices: uint256 = self.price_scale_packed

for k in range(N_COINS-1):

price_scale[k] = bitwise_and(packed_prices, PRICE_MASK) # * PRICE_PRECISION_MUL

packed_prices = shift(packed_prices, -PRICE_SIZE)

precisions: uint256[N_COINS] = PRECISIONS

xp[0] *= PRECISIONS[0]

for k in range(1, N_COINS):

xp[k] = xp[k] * price_scale[k-1] * precisions[k] / PRECISION

prec_i: uint256 = precisions[i]

# Recalculate A and gamm when they are ramping

if True:

t: uint256 = self.future_A_gamma_time

if t > 0:

x0 *= prec_i

if i > 0:

x0 = x0 * price_scale[i-1] / PRECISION

x1: uint256 = xp[i] # Back up old value in xp

xp[i] = x0

self.D = Math(math).newton_D(A_gamma[0], A_gamma[1], xp)

xp[i] = x1 # And restore

if block.timestamp >= t:

self.future_A_gamma_time = 1

prec_j: uint256 = precisions[j] # cache the presision of token_out

# newton_y is the newton's method to calculate xp_out (value, not amount)

# dy is the difference between after and before of xp_out

dy = xp[j] - Math(math).newton_y(A_gamma[0], A_gamma[1], xp, self.D, j)

xp[j] -= dy

# To prevent the loss of precision of the subsequent division operation (LP interests are preferred)

dy -= 1

# Convert value to amount (dy/price), when token_out is not coin[0]

if j > 0:

dy = dy * PRECISION / price_scale[j-1]

dy /= prec_j

dy -= self._fee(xp) * dy / 10**10 # cost fees on token_out

assert dy >= min_dy, "Slippage" # If amount_out < min_amount_out after cost fees, revert

y -= dy

self.balances[j] = y # update balances of reserves

# Transfer token_out to user

if j == 2 and use_eth:

WETH(coins[2]).withdraw(dy)

raw_call(msg.sender, b"", value=dy)

else:

ERC20(_coins[j]).transfer(msg.sender, dy)

# update xp

y *= prec_j

if j > 0: # If not coin[0], multiply price get value

y = y * price_scale[j-1] / PRECISION

xp[j] = y

# calculate price, pass it to tweak_price as last_price input

# There three kind of case:

# 1. token_in and token_out both are not coins[0], p = amount_in * price / amount_out

# 2. 3. one of token_in and token_out is coins[0], using coin[0] as the dividend

# Notice: dx and dy both are amount, not value

if dx > 10**5 and dy > 10**5:

_dx: uint256 = dx * prec_i

_dy: uint256 = dy * prec_j

if i != 0 and j != 0:

p = bitwise_and(

shift(self.last_prices_packed, -PRICE_SIZE * convert(i-1, int256)),

PRICE_MASK

) * _dx / _dy # * PRICE_PRECISION_MUL

elif i == 0:

p = _dx * 10**18 / _dy

else: # j == 0

p = _dy * 10**18 / _dx

ix = i

self.tweak_price(A_gamma, xp, ix, p, 0)

log TokenExchange(msg.sender, i, dx, j, dy)

return dyfees

根据 xp 动态计算当前手续费水平,规则参照 Dynamic fees 的公式。

@internal

@view

def _fee(xp: uint256[N_COINS]) -> uint256:

# f is the g in the formula

f: uint256 = Math(math).reduction_coefficient(xp, self.fee_gamma)

return (self.mid_fee * f + self.out_fee * (10**18 - f)) / 10**18

@external

@view

def fee() -> uint256:

return self._fee(self.xp())

@external

@view

def fee_calc(xp: uint256[N_COINS]) -> uint256:

return self._fee(xp)reduction_coefficient() 是 CurveCryptoMath 合约中用于计算 g 的函数,参见 CurveCryptoMath#reduction_coefficient()

Fees of add liquidity imbalanced

上一章中提到如果用户不平衡的操作流动性,Curve 会对其部分流动性收取手续费,接下来我们将详细探究其运作逻辑。

Sdiff/S

假设现在用户 A 向 tricrypto 池中添加一笔不平衡的流动性,该添加操作 USDT-WBTC-WETH 增加的 xp 分别有 [100, 200, 300] (计算时都会将 balance 乘以 price ,为了简化问题,我们直接假设 xp 的增加数值)。这笔不平衡的添加,会让 USDT 和 WETH 的价值相差更大,所以我们需要累加这些引发偏离平衡的量来计算手续费。在 v2 CryptoSwap 中具体的逻辑如下:

- 计算该笔添加的总价值

S = sum(xp) - 计算该笔添加的平均价值

avg = S / N - 累加每种资产添加价值与 avg 偏差量

Sdiff = sum(|xp - avg|),注意是累加差的绝对值 - 将 Sdiff 和 S 的比值作为手续费的调整系数,直接在操作用户的 LP token 中扣除

所以 添加/移除 的越不平衡,手续费将收取的越多,反过来,如果添加的每种资产价值相等,则不会收取手续费。

那么添加 [100, 200, 300] 的情况如下:

S = 100 + 200 + 300 = 600

avg = 600 / 3 = 200

Sdiff = |100 - 200| + |200 - 200| + |300 - 200| = 200最后我们得到了手续费的调整系数 Sdiff/S = 200/600。

N/(4*(N-1))

除了 Sdiff / S 这个与不平衡程度相关的调整系数,流动性操作计算手续费还有一个和 N 相关的调整系数 N / (4 * (N - 1))。

因为 N 越小,每种资产的价格受到不平衡的影响越大,N 越大每种资产价格受到不平衡的影响反而越小。该调整系数的值处于区间 [1/2, 1/4) 。

- 当 N = 2 时,系数最大,为

2 / (4 * (2 - 1)) = 1/2 - 当 N 趋近于无穷大时,系数最小,

calculate token fee

在 v2 CryptoSwap 中,_calc_token_fee() 函数是根据流动性变化量的不平衡程度和 N 相关的系数计算手续费率的函数,入参 amounts 是流动性变化的量(增加或减少)。例如添加流动性,则考虑的是本次操作每种资产分别增加了多少 xp,注意这里是 xp,不是数量。

函数将返回调整后的手续费率,用于直接在 LP token 上扣除手续费。

fee_rate = fee_rate_base * (Sdiff / S) * N / (4 * (N - 1))接下来我们看看如何具体的实现这一计算过程:

- 首先计算 xp 的改变量,计算增加或减少的绝对值,存入

amountsp数组 - 将

amountsp传入_calc_token_fee()函数- 根据池子现有 xp 利用

fee(xp)函数计算交易的基准费率,注意此时 xp 已经根据amountsp调整过 - 费率乘以系数

N / (4 * (N - 1)) - 计算

amountsp的总和S - 计算

amountsp的累加偏差量Sdiff - 最后费率再乘以系数

Sdiff / S

- 根据池子现有 xp 利用

- 至此我们得到了一个考虑了 N 的数值和流动性操作的不平衡程度的调整后的费率

- 最后直接在 LP token 的数量扣除,将价值留在池子内部,就完成了不平衡流动性的手续费收取

# amountsp is an array of delta xp of every coin,

# it is _calc_token_fee() input params `amounts`.

# notice: amountsp here is xp, the product of price and balance

for i in range(N_COINS):

if amounts[i] > 0:

amountsp[i] = xp[i] - xp_old[i]

...

# according to the degree of imbalance and the coefficient of N calculate fee_rate

# notice: amounts is amountsp

@view

@internal

def _calc_token_fee(amounts: uint256[N_COINS], xp: uint256[N_COINS]) -> uint256:

# fee = sum(amounts_i - avg(amounts)) * fee' / sum(amounts)

fee: uint256 = self._fee(xp) * N_COINS / (4 * (N_COINS-1))

S: uint256 = 0

for _x in amounts:

S += _x

avg: uint256 = S / N_COINS

Sdiff: uint256 = 0

for _x in amounts:

if _x > avg:

Sdiff += _x - avg

else:

Sdiff += avg - _x

return fee * Sdiff / S + NOISE_FEE

# we cost fee directly on d_token which is

# the number of LP token that user will get

d_token_fee = self._calc_token_fee(amountsp, xp) * d_token / 10**10 + 1

...calc_token_fee

计算不平衡的添加流动性时,过程中产生的交易手续费。amounts 是 xp 的增量, xp 是当前 xp,返回添加流动性过程中产生的手续费。

注意: 返回手续费的单位是以 LP token 为计量的,该数量将直接在 mint 出来的 LP token 数量上相减,参见 add_liquidity 的代码

- 计算增加价值

S和平均数avg - 每个资产增量和 avg 的差量取绝对值累加作为

Sdiff fee = sum(amounts_i - avg(amounts)) / sum(amounts) * fee'- 按照不平衡部分和总增量的比例来收取

- 观察整个过程的运算单位,最后是

Sdiff(价值) /S(价值),两个价值单位被抵消,固最后的得数是一个比例(无单位),因为该函数将被用于计算 LP token 手续费扣减数量 NOISE_FEE是噪音参数,极小的值,但使得返回值不能为零,防止可能的攻击

@view

@internal

def _calc_token_fee(amounts: uint256[N_COINS], xp: uint256[N_COINS]) -> uint256:

# fee = sum(amounts_i - avg(amounts)) * fee' / sum(amounts)

fee: uint256 = self._fee(xp) * N_COINS / (4 * (N_COINS-1))

S: uint256 = 0

for _x in amounts:

S += _x

avg: uint256 = S / N_COINS

Sdiff: uint256 = 0

for _x in amounts:

if _x > avg:

Sdiff += _x - avg

else:

Sdiff += avg - _x

return fee * Sdiff / S + NOISE_FEE

@external

@view

def calc_token_fee(amounts: uint256[N_COINS], xp: uint256[N_COINS]) -> uint256:

return self._calc_token_fee(amounts, xp)Fees of remove liquidity imbalanced

calc_withdraw_one_coin

计算移除流动性只收取单一资产,可以收到的具体资产数量

- 在 D 值上扣除手续费,而不是输出资产 y,即,直接减少用户可赎回的 LP token 作为手续费

- dD 是根据移除 LP token 和 totalSupply 比例计算的 delta D

- 先在 dD 上扣除手续费,其逻辑是直接向 dD 的一半收取手续费,因为此时是赎回单一资产,相当于其中一半需要用其他资产交易成该资产,所以直接 / 2

- 根据新的 D 值使用牛顿法计算出该资产的数量 y

curve v2 不平衡的移除流动性只有获取单一资产的接口,对于手续费的调整系数直接简化为 1/2,而非

N/(4*(N-1))

@internal

@view

def _calc_withdraw_one_coin(A_gamma: uint256[2], token_amount: uint256, i: uint256, update_D: bool,

calc_price: bool) -> (uint256, uint256, uint256, uint256[N_COINS]):

token_supply: uint256 = CurveToken(token).totalSupply()

assert token_amount <= token_supply # dev: token amount more than supply

assert i < N_COINS # dev: coin out of range

xx: uint256[N_COINS] = self.balances # cache balances

xp: uint256[N_COINS] = PRECISIONS # xp container, cache precision and mutiply price later

D0: uint256 = 0 # cache D value

# calculate xp = balances * price

price_scale_i: uint256 = PRECISION * PRECISIONS[0]

if True: # To remove packed_prices from memory

packed_prices: uint256 = self.price_scale_packed

xp[0] *= xx[0]

for k in range(1, N_COINS):

p: uint256 = bitwise_and(packed_prices, PRICE_MASK) # * PRICE_PRECISION_MUL

if i == k:

price_scale_i = p * xp[i]

xp[k] = xp[k] * xx[k] * p / PRECISION

packed_prices = shift(packed_prices, -PRICE_SIZE)

# Use newton's method to update D

if update_D:

D0 = Math(math).newton_D(A_gamma[0], A_gamma[1], xp)

else:

D0 = self.D

D: uint256 = D0

# Charge the fee on D, not on y, e.g. reducing invariant LESS than charging the user

fee: uint256 = self._fee(xp)

dD: uint256 = token_amount * D / token_supply

D -= (dD - (fee * dD / (2 * 10**10) + 1))

y: uint256 = Math(math).newton_y(A_gamma[0], A_gamma[1], xp, D, i)

dy: uint256 = (xp[i] - y) * PRECISION / price_scale_i

xp[i] = y

# Calculate price of this trade,pass it to tweak_price.

# The logic is simular with add liquidity

p: uint256 = 0

if calc_price and dy > 10**5 and token_amount > 10**5:

# p_i = dD / D0 * sum'(p_k * x_k) / (dy - dD / D0 * y0)

S: uint256 = 0

precisions: uint256[N_COINS] = PRECISIONS

last_prices: uint256[N_COINS-1] = empty(uint256[N_COINS-1])

packed_prices: uint256 = self.last_prices_packed

for k in range(N_COINS-1):

last_prices[k] = bitwise_and(packed_prices, PRICE_MASK) # * PRICE_PRECISION_MUL

packed_prices = shift(packed_prices, -PRICE_SIZE)

for k in range(N_COINS):

if k != i:

if k == 0:

S += xx[0] * PRECISIONS[0]

else:

S += xx[k] * last_prices[k-1] * precisions[k] / PRECISION

S = S * dD / D0

p = S * PRECISION / (dy * precisions[i] - dD * xx[i] * precisions[i] / D0)

return dy, p, D, xp

@view

@external

def calc_withdraw_one_coin(token_amount: uint256, i: uint256) -> uint256:

return self._calc_withdraw_one_coin(self._A_gamma(), token_amount, i, True, False)[0]Compare with v1 StableSwap in imbalanced liquidity

在 v1 StableSwap 中,对于不平衡的流动性计算手续费和 v2 CryptoSwap 有所不同。

- 计算流动性改变后的 balances,然后用

new_balances代入牛顿法中计算出新的 D 值 D1 - 根据

D1/D0即 D 的变化比例,同比放大每种资产的 balance,得出ideal_balance

同样以添加流动性为例,v1 StableSwap 涉及到不平衡流动性手续费的代码如下:

# 3pool.vy

@external

@nonreentrant('lock')

def add_liquidity(amounts: uint256[N_COINS], min_mint_amount: uint256):

...

# fee_rate multiple coefficient on N

_fee: uint256 = self.fee * N_COINS / (4 * (N_COINS - 1))

# add amounts on balances get new_balances

for i in range(N_COINS):

in_amount: uint256 = amounts[i]

new_balances[i] = old_balances[i] + in_amount

...

# calculate new D by new_balances as D1

# D0 is D old value

D1: uint256 = self.get_D_mem(new_balances, amp)

assert D1 > D0

# Only account for fees if we are not the first to deposit

for i in range(N_COINS):

ideal_balance: uint256 = D1 * old_balances[i] / D0

difference: uint256 = 0

if ideal_balance > new_balances[i]:

difference = ideal_balance - new_balances[i]

else:

difference = new_balances[i] - ideal_balance

fees[i] = _fee * difference / FEE_DENOMINATOR

...